4. July 2018

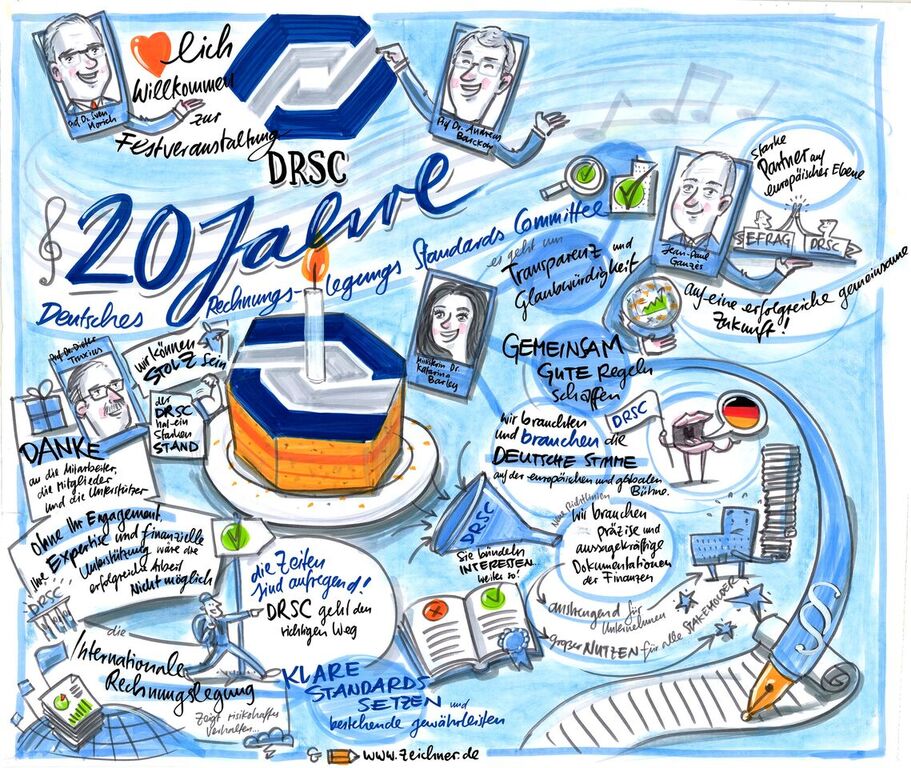

20 years DRSC – Festive anniversary event

On 2 July 2018, the German accounting standard-setter ASCG celebrated 20 years of its existence. On this occasion, we had invited around 200 guests from Germany and abroad to a festive event at the Allianz Forum in Berlin.

We were honoured by prominent speakers from the business community, NGOs and politics, who gave inspiring contributions and opinions through greeting words, a keynote speech and by participating in two panel discussions. While a reception in front of a metropolitan backdrop formed the (suitable) frame for the afternoon, technical and political aspects around the field of corporate reporting were the focus of the event.

In his greeting, Prof Dieter Truxius, Vice Chair-man of the Administrative Board, proudly thanked the ASCG for its work. He emphasized that the ASCG is the body in which all stakeholders work actively together, which is why the ASCG is rightly perceived the eyes and ears and the voice of the entire German economy in accounting matters.

Next, Minister Dr Katarina Barley from the Federal Ministry of Justice and Consumer Protection (BMJV) honoured us with her greeting word. She highlighted the ASCG as a good example of how business and politics worked together. Prof Morich thanked the BMJV for their many years of trust in the ASCG’s work.

Jean-Paul Gauzès, President of the EFRAG Board, also welcomed the ASCG and its guests. He referred to the very good and close cooperation between ASCG and EFRAG since its inception. He also pointed out recent developments at EFRAG and asked for continued intensive German participation.

In her keynote speech, Melanie Kreis, Chief Financial Officer of Deutsche Post AG, high-lighted the biggest current challenges of corporate reporting. In addition to a particular vocal plea for uniform global accounting standards, a request was also made that standard-setters should consider the practical effects on business models and corporate management in any theoretical considerations early on (and even more).

After a coffee break, the event continued with two panel discussions featuring top notch speakers.

The first motto “Changing values: managing behaviour through CSR reporting” raised the question of where the purpose of the financial report ends. The four panelists digged into the tension area of needing legal regulation versus the power of self-regulation in respect of corporate reporting. During the discussion, it was lively debated whether, and to what extent, transparency about CSR issues can influence that behaviour effectively. In addition, it became clear that transparency also pursues the goal of comparability, which should not, however, lead to uniformity. Otherwise, the management perspective would hardly be given any room.

In the second panel, entitled “Technological Change: Digital Reporting vs. Reporting in a Digital World”, participants discussed the multiple influence of technological changes to the content of corporate reporting as well as on nature and its form and means. During this panel discussion, it was emphasised that digitalisation leads to new, mainly intangbigle assets for which new accounting concepts are presumably needed. With regard to form and scope of reporting, technological change was seen as likely leading to considerably more possibilities for both providing and using information. This again underlined the con-troversy about standardisation and comparability – even though the participants did not come forward with proposals for a universal solution.

In his closing remarks, Prof Morich conceded that the standard-setters and in particular the ASCG will not run out of topics and challenges; the ASCG will continue to devote itself to them with expert knowledge and continued enthusiasm.